Travel insurance generally covers only emergency or urgent medical expenses, according to the California state insurance commission, which regulates policies in the state.

This article was published on Thursday, November 18, 2021 in Kaiser Health News.

Duy Hoa Tran, a retired Vietnamese schoolteacher, arrived in Los Angeles in February 2020 to visit his daughter and 2-month-old grandson. Two weeks later, the door closed behind him. To prevent the spread of covid-19, Vietnam shut its borders. No commercial flights would be allowed into the country for the next 18 months.

Tran’s daughter, An Tran, who has a doctorate in business administration and teaches marketing at the University of La Verne in California, did what she thought was necessary to ensure medical coverage for her then-65-year-old father during the pandemic. But the only option for a visitor on a tourist visa was travel insurance. In early March 2020, An Tran found and purchased a policy, for about $350 a month, from a company called Seven Corners.

She might as well not have bothered.

The elder Tran had been staying at An’s home in Diamond Bar, California, about a year when he told his daughter he was having trouble seeing out of his right eye. A visit to an ophthalmologist produced a solemn verdict: Tran had severe glaucoma and would quickly go blind unless he got surgery.

Seven Corners gave written preapproval for the procedures recommended by Dr. Brian Chen. To be safe, An Tran called the insurer “many times” to confirm it would cover the expense, but no one she spoke with would give her a definitive answer, she said. Chen, however, assured An that insurance companies typically covered the treatment, which was pretty routine.

On April 19, Tran underwent the first of three eye surgeries to resolve the glaucoma. The surgeries — the last was on July 19 — were successful. And then on Aug. 5, Seven Corners sent An Tran a denial of service letter.

The company’s policy excluded coverage for any “preexisting condition,” by which it meant any condition “whether or not previously manifested, symptomatic, known, diagnosed, treated or disclosed,” the letter said.

An Tran and her father were on the hook for nearly $38,000 in medical bills, although Seven Corners had preauthorized the surgery and she had paid around $6,000 for the insurance over the previous year and a half.

As for the bill, “my dad obviously can’t pay it,” Tran said. His $260 monthly pension from the Vietnamese government isn’t enough even for him to live on in Vietnam, she said.

The surgical procedures Duy Hoa Tran received are quite routine in the United States, said Dr. Davinder Grover, an ophthalmologist in the Dallas area and clinical spokesperson for the American Academy of Ophthalmology.

Medicare would generally pay about a quarter of the $37,896.83 Tran was billed for the surgeries, Grover said. If Tran’s daughter had known beforehand that insurance wouldn’t cover the procedures, the physician’s practice might have been willing to charge something like $12,000, he said.

The policy An Tran purchased had no deductible and offered coverage of up to $100,000 in medical bills, including covid care. But travel insurance generally covers only emergency or urgent medical expenses, according to the California state insurance commission, which regulates policies in the state.

Megan Moncrief, chief marketing officer for Squaremouth, which aggregates various companies’ travel insurance plans — including some from Seven Corners — and offers them through its website, said the policy language was not unusual for travel insurance. She noted the policy’s stipulation that it covered some acute conditions only if the patient sought treatment within 24 hours of the initial symptoms.

Moncrief said the fact that Tran did not seek treatment immediately may be the reason his surgeries weren’t covered. (Seven Corners refused all comment on the case.) She acknowledged it was hardly surprising he hadn’t dashed to the doctor at the first sign of discomfort: “I don’t know that I would have done that either, if I just had blurry vision.”

As for Seven Corners’ refusal to pay despite precertification, this is not uncommon, she said. By precertifying, the insurer verifies that a procedure is a covered benefit but doesn’t guarantee the insurer will cover it for that particular patient.

Travel insurance typically offers little protection for any health problem linked to a preexisting condition, regardless of whether that condition has ever been diagnosed, says Susan Yates, general manager in the U.S. for Falck Global Assistance, an international insurer.

“For visitors to the U.S., especially those who are not permanent residents or citizens, it can be difficult to obtain health insurance,” she said. The Affordable Care Act doesn’t cover tourists, though some resident noncitizens can buy coverage.

“It’s usually better for a visitor to buy travel insurance from their country of origin, but in some countries (Vietnam being one), the insurance market is not developed,” Yates wrote in an email.

Tran had tried unsuccessfully for months to fly home to his town near Ho Chi Minh City, where his wife lives with another grandchild. On 14 occasions, An bought him tickets on regular commercial flights that were subsequently canceled. He was also unable to get a seat on charter flights arranged by the Vietnamese government; those tickets generally were available only through third parties charging up to $10,000.

The eye surgeon, Chen, offered to discuss the case with KHN, but his medical group’s counsel said it had a policy against discussing insurance issues with reporters, even with the patient’s consent.

After KHN approached him to discuss the issue, Chen told An Tran that he was waiving his $8,144 fee for the surgeries. The Acuity Eye Group, where he practices, would not immediately confirm Chen’s offer, but told An Tran they were seeking approvals to waive his fee and all other charges as well.

On Sept. 15, Duy Hoa Tran finally managed to get on a charter flight back to Vietnam. He’s happy to be home, An Tran said.

Routine immunizations protect children against 16 infectious diseases, including measles, diphtheria, and chickenpox, and inhibit transmission to the community; the rollout of covid shots for younger kids is an opportunity to catch up on routine vaccinations.

This article was published on Thursday, November 18, 2021 in Kaiser Health News.

WESTMINSTER, Colo. — Melissa Blatzer was determined to get her three children caught up on their routine immunizations on a recent Saturday morning at a walk-in clinic in this Denver suburb. It had been about a year since the kids’ last shots, a delay Blatzer chalked up to the pandemic.

Two-year-old Lincoln Blatzer, in his fleece dinosaur pajamas, waited anxiously in line for his hepatitis A vaccine. His siblings, 14-year-old Nyla Kusumah and 11-year-old Nevan Kusumah, were there for their TDAP, HPV and meningococcal vaccines, plus a covid-19 shot for Nyla.

“You don’t have to make an appointment and you can take all three at once,” said Blatzer, who lives several miles away in Commerce City. That convenience outweighed the difficulty of getting everyone up early on a weekend.

Child health experts hope community clinics like this, along with the return to in-person classes, more well-child visits and the rollout of covid shots for younger children, can help boost routine childhood immunizations, which dropped during the pandemic. Despite a rebound, immunization rates are still lower than in 2019, and disparities in rates between racial and economic groups, particularly for Black children, have been exacerbated.

“We’re still not back to where we need to be,” said Dr. Sean O’Leary, a pediatric infectious-disease doctor at Children’s Hospital Colorado and a professor of pediatrics at the University of Colorado School of Medicine.

Routine immunizations protect children against 16 infectious diseases, including measles, diphtheria and chickenpox, and inhibit transmission to the community.

The rollout of covid shots for younger kids is an opportunity to catch up on routine vaccinations, said O’Leary, adding that children can receive these vaccines together. Primary care practices, where many children are likely to receive the covid shots, usually have other childhood vaccines on hand.

“It’s really important that parents and health care providers work together so that all children are up to date on these recommended vaccines,” said Dr. Malini DeSilva, an internist and pediatrician at HealthPartners in the Minneapolis-St. Paul area. “Not only for the child’s health but for our community’s health.”

People were reluctant to come out for routine immunizations at the height of the pandemic, said Karen Miller, an immunization nurse manager for the Denver area’s Tri-County Health Department, which ran the Westminster clinic. National and global data confirm what Miller saw on the ground.

Global vaccine coverage in children fell from 2019 to 2020, according to a recent study by scientists at the Centers for Disease Control and Prevention, the World Health Organization and UNICEF. Reasons included reduced access, lack of transportation, worries about covid exposure and supply chain interruptions, the study said.

Third doses of the diphtheria, tetanus and whooping cough (DTP) vaccine and of the polio vaccine decreased from 86% of all eligible children in 2019 to 83% in 2020, according to the study. Worldwide, 22.7 million children had not had their third dose of DTP in 2020, compared with 19 million in 2019. Three doses are far more effective than one or two at protecting children and communities.

In the United States, researchers who studied 2019 and 2020 data on routine vaccinations in California, Colorado, Minnesota, Oregon, Washington and Wisconsin found substantial disruptions in vaccination rates during the pandemic that continued into September 2020. For example, the percentage of 7-month-old babies who were up to date on vaccinations decreased from 81% in September 2019 to 74% a year later.

The proportion of Black children up to date on immunizations in almost all age groups was lower than that of children in other racial and ethnic groups. This was most pronounced in those turning 18 months old: Only 41% of Black children that age were caught up on vaccinations in September 2020, compared with 57% of all children at 18 months, said DeSilva, who led that study.

A CDC study of data from the National Immunization Surveys found that race and ethnicity, poverty and lack of insurance created the greatest disparities in vaccination rates, and the authors noted that extra efforts are needed to counter the pandemic’s disruptions.

In addition to the problems caused by covid, Miller said, competing life priorities like work and school impede families from keeping up with shots. Weekend vaccination clinics can help working parents get their children caught up on routine immunizations while they get a flu or covid shot. Miller and O’Leary also said reminders via phone, text or email can boost immunizations.

“Vaccines are so effective that I think it’s easy for families to put immunizations on the back burner because we don’t often hear about these diseases,” she said.

It’s a long and nasty list that includes hepatitis A and B, measles, mumps, whooping cough, polio, rubella, rotavirus, pneumococcus, tetanus, diphtheria, human papillomavirus and meningococcal disease, among others. Even small drops in vaccination coverage can lead to outbreaks. And measles is the perfect example that worries experts, particularly as international travel opens up.

“Measles is among the most contagious diseases known to humankind, meaning that we have to keep very high vaccination coverage to keep it from spreading,” said O’Leary.

In 2019, 22 measles outbreaks occurred in 17 states in mostly unvaccinated children and adults. O’Leary said outbreaks in New York City were contained because surrounding areas had high vaccination coverage. But an outbreak in an undervaccinated community still could spread beyond its borders, he said.

In some states a significant number of parents were opposed to routine childhood vaccines even before the pandemic for religious or personal reasons, posing another challenge for health professionals. For example, 87% of Colorado kindergartners were vaccinated against measles, mumps and rubella during the 2018-19 school year, one of the nation’s lowest rates.

Those rates bumped up to 91% in 2019-20 but are still below the CDC’s target of 95%.

O’Leary said he does not see the same level of hesitancy for routine immunizations as for covid. “There has always been vaccine hesitancy and vaccine refusers. But we’ve maintained vaccination rates north of 90% for all routine childhood vaccines for a long time now,” he said.

Malini said the “ripple effects” of missed vaccinations earlier in the pandemic continued into 2021. As children returned to in-person learning this fall, schools may have been the first place families heard about missed vaccinations. Individual states set vaccination requirements, and allowable exemptions, for entry at schools and child care facilities. Last year, Colorado passed a school entry immunization law that tightened allowable exemptions.

“Schools, where vaccination requirements are generally enforced, are stretched thin for a variety of reasons, including covid,” said O’Leary, adding that managing vaccine requirements may be more difficult for some, but not all, schools.

Anayeli Dominguez, 13, was at the Westminster clinic for a TDAP vaccine because her middle school had noticed she was not up to date.

“School nurses play an important role in helping identify students in need of immunizations, and also by connecting families to resources both within the district and in the larger community,” said Denver Public Schools spokesperson Will Jones.

In September, when Shelly Azzopardi went to Wellstar Kennestone Hospital with abdominal pain, she didn’t worry about her insurance.

Doctors said she had a case of appendicitis. But she also tested positive at the hospital in Marietta, Georgia, for covid-19. Physicians decided not to do surgery and treated her with antibiotics and painkillers. Azzopardi, 47, went home after a couple of days in the hospital, feeling better.

But in October, the appendix pain again flared. Her husband took her to the same hospital, where surgery was performed successfully. This time, though, she ran into a snag with her insurance.

Azzopardi has UnitedHealthcare coverage, and as of Oct. 3, Wellstar Health System was no longer in the giant insurer’s network, after the two sides did not agree on a new contract.

Wellstar dominates the Cobb County area where Azzopardi and her husband live. She has applied to UnitedHealthcare for a “continuity of care” waiver, which would extend her previous in-network coverage for the treatment of an ongoing condition for the October hospital visit and surgery. If it doesn’t work out, she could owe thousands of dollars. “I don’t know where it stands,” Azzopardi said.

On a larger level, the severed contract between a hospital system and health insurer reflects tensions that have been growing nationally this year. In the past, even when contract negotiations became publicly antagonistic, they typically would be resolved before the deadline for termination.

Now health care consultants and industry officials say an increasing number of contracts end without a deal. Even if they are eventually resolved, those terminations throw tens of thousands of patients into the difficult position of choosing between much higher out-of-pocket costs or leaving a trusted physician and hospital.

The Wellstar vs. UnitedHealthcare situation — and an even bigger dispute looming in metro Atlanta involving Anthem Blue Cross and Blue Shield — come at a tricky time, during open enrollment season when many employers have already picked their insurance offerings and many consumers must choose their health plan.

“We are seeing more insurers terminate contracts without a deal, and this is both a national and local trend,” said Beth Spoto, a Georgia-based health care consultant with Spoto & Associates. From the insurers’ point of view, she said, it’s a hardball tactic to lower payment rates to medical providers for services.

“Health systems are getting quite large, so you are dealing with hundreds of millions of dollars,” she said. “The fighting is getting pretty tough.”

Recent contract terminations involving big insurers include UnitedHealthcare vs. Montefiore Health System in New York, and Anthem vs. Dignity Health in California. Each conflict was eventually resolved, though Montefiore took several months to settle.

Hospitals are reporting higher tensions in negotiations with health insurers, said Molly Smith, an American Hospital Association vice president. She said contract talks often are not conducted by local executives of the insurer, which might allow for more collaboration, but are directed instead by company headquarters.

Just in the Atlanta area, other out-of-network situations involving insurance heavyweights UnitedHealthcare and Anthem have occurred in the past couple of years. Northside Hospital’s Gwinnett County facilities were out of network for UnitedHealthcare members for five months, while Northeast Georgia Health System in Gainesville left Anthem’s lineup for three months.

In the most recent dispute, Wellstar said it wants UHC to pay reimbursements similar to those it gets from other insurers. UnitedHealthcare, based in Minnesota, counters that Wellstar wants “egregious” rate hikes that the insurer said would amount to 37% over three years.

“Both sides said the other is just out for money,” Azzopardi said. The impasse, she said, “is cruel to the patients who have done nothing wrong.”

The open enrollment quandary has Emilie Cousineau of Smyrna, Georgia, wondering whether to stay with UnitedHealthcare or switch to Anthem, which she said would cost her more for the upcoming benefits year in her employer plan.

Cousineau canceled a Wellstar well-check appointment recently because suddenly it was out of network. “Right now, it’s an inconvenience.” But her doctor as well as her kids’ pediatrician are Wellstar physicians. “I’m picky about my health care,” she said.

Uncertainty over covid and rising hospital labor costs are fueling the disruptions, consultants said.

Health insurers recorded sky-high profits last year as people avoided medical care because of fears about covid. This year, profits have been lower but still healthy. For hospitals, the pandemic brought mixed results. Some richer, bigger health systems racked up huge surpluses, helped by covid relief funds, while many safety-net and rural hospitals fought hard to break even.

Cole Manbeck, a spokesperson for UnitedHealthcare, said affordability of health care is of prime importance to consumers and employers. They expect the insurer to help contain costs, which requires maintaining fair and competitive agreements with hospitals and doctors in its network, he said.

Insurers also point out that health care systems have enhanced their bargaining clout by acquiring additional hospitals and doctor practices. The tough negotiations extend to physician group contracts, said Dave Smith with the health care consulting firm Kearny Street Management. Insurers, he said, “are trying to drive health care costs down, and are doing it on the backs of physicians and hospitals.”

Factoring into the fray are payment delays involving insurers Anthem and UnitedHealthcare. Hospitals are dealing with a spike in retroactive claim denials by UnitedHealthcare for emergency department care, the AHA’s Smith said.

KHN also recently reported that Anthem Blue Cross is behind on billions of dollars in payments owed to hospitals and doctors because of onerous new reimbursement rules, computer problems and mishandled claims, according to hospital officials in multiple states.

Tom Mee, CEO of North Country Healthcare in New Hampshire, said the outstanding claims owed to his system by Anthem rose $250,000 in one quarter to reach $1 million.

Indianapolis-based Anthem said the contract rifts and the claims issue are not related. Both it and UnitedHealthcare noted that the large majority of contracts are renewed without public attention.

Employers, meanwhile, don’t like these network disruptions, said Ash Shehata, a health care consultant with KPMG. But, he added, employers also don’t want to subsidize the rate increases.

“When times are good, and everybody is doing well, generally you don’t see these negotiation issues,” he said. “As long as the environment remains unpredictable, we’ll see some unpredictable negotiations.”

Contract terminations harm hospitals more than insurers, said Nathan Kaufman of Kaufman Strategic Advisors. For example, UnitedHealthcare and Anthem, which operate in several states, “can take a hit in one state,” he said, because they’re diversified and insurers still receive premium payments for members after a contract with a hospital lapses.

“On day one, the hospitals start feeling increased financial stress,” Kaufman said. “They experience this financial jolt.”

The Atlanta market is facing another such contract disruption. Anthem has alerted consumers that Northside Hospital and its facilities may not be part of its network come Jan. 1. While the Wellstar vs. UnitedHealthcare tug-of-war involves an estimated 80,000 consumers, the Northside contract could affect four or five times that many, according to Northside officials.

“Anthem’s timing is very unfavorable to our patients,” said Lee Echols, a Northside spokesperson. “It’s hard to understand. We’re still in a pandemic, and this is the open enrollment period for health care policyholders. Many people are returning to their physicians and hospitals for deferred care, and Anthem’s threats make that process really challenging.”

But Anthem spokesperson Christina Gaines said that the company is fighting to curb health care costs, and that Northside is one of the most expensive systems in Georgia.

The showdown has consumers such as Carol Lander of Sandy Springs, Georgia, concerned and confused.

She has been an Anthem member for years and has used nearby Northside facilities and doctors. She’s now shopping for other plans to see if they include Northside in their networks. One insurance plan has her doctor but not her sons’ physician.

“It’s so frustrating,” said Lander. “This is a huge deal in this area.”

Congress passed the No Surprises Act last December to shield patients from unexpected bills, but now many doctors, their medical associations, and members of Congress are fighting a new policy that favors insurers and doesn’t follow the spirit of the legislation.

This article was published on Wednesday, November 17, 2021 in Kaiser Health News.

The detente that allowed Congress to pass a law curbing surprise medical bills has disintegrated, with a bipartisan group of 152 lawmakers assailing the administration’s plan to regulate the law and medical providers warning of grim consequences for underserved patients.

For years, people have faced these massive, unexpected bills when they get treatment from hospitals or doctors outside their insurance company’s network. It often happens when patients seek care at an in-network hospital but a physician such as an emergency room doctor or anesthesiologist who treats the patient is not covered by the insurance plan. The insurer would pay only a small part of the bill, and the unsuspecting patient would be responsible for the balance.

Congress passed the No Surprises Act last December to shield patients from that experience after long, hard-fought negotiations with providers and insurers finally yielded an agreement that lawmakers from both parties thought was fair: a 30-day negotiation period that would be followed by arbitration when agreements cannot be reached.

The rule, which would take effect in January, effectively leaves patients out of the fight. Providers and insurers have to work it out among themselves, following the new policy.

But now many doctors, their medical associations and members of Congress are crying foul, arguing the rule released by the Biden administration in September for implementing the law favors insurers and doesn’t follow the spirit of the legislation.

“The Administration’s recently proposed regulation to begin implementing the law does not uphold Congressional intent and could incentivize insurance companies to set artificially low payment rates, which would narrow provider networks and potentially force small practices to close thus limiting patients access to care,” Rep. Larry Bucshon (R-Ind.), who is a doctor and helped spearhead a letter of complaint this month, said in a statement to KHN.

Nearly half of the 152 lawmakers who signed that letter were Democrats, and many of the physicians serving in the House signed it. But the backlash has not won the support of some powerful Democrats, including Rep. Frank Pallone (N.J.), chair of the Energy and Commerce Committee, and Sen. Patty Murray (Wash.), chair of the Senate Health, Energy, Labor and Pensions Committee, who wrote to the administration urging officials to move forward with their plan.

Some members of Congress who are also doctors held a conference call with the administration late last month to complain, according to aides to lawmakers on Capitol Hill, who could not speak on the record because they did not have authorization to do so. “The doctors in Congress are furious about this,” said one staff member familiar with the call. “They very clearly wrote the law the way that they did after a year, or two years, of debate over which way to go.”

The controversy pertains to a section of the proposed final regulations focusing on arbitration.

The lawmakers’ letter — organized by Reps. Thomas Suozzi (D-N.Y.), Brad Wenstrup (R-Ohio), Raul Ruiz (D-Calif.) and Bucshon — noted that the law specifically forbids arbitrators to favor a specific benchmark to determine what providers should be paid. Expressly excluded are the rates paid to Medicare and Medicaid, which tend to be lower than insurance company rates, and the average rates that doctors bill, which tend to be much higher.

Arbitrators would be instructed to consider the median in-network rates for services as one of several factors in determining a fair payment. They would also have to consider items such as a physician’s training and quality of outcomes, local market share of the parties involved where one side may have outsize leverage, the patient’s understanding and complexity of the services, and past history, among other things.

But the proposed rule doesn’t instruct arbiters to weigh those factors equally. It requires them to start with what’s known as the qualifying payment amount, defined as the median rate the insurer pays in-network providers for similar services in the area.

If a physician thinks they deserve a better rate, they are then allowed to point to the other factors allowed under the law — which the medical practitioners in Congress believe is contrary to the bill they wrote.

The provisions in the new rule “do not reflect the way the law was written, do not reflect a policy that could have passed Congress, and do not create a balanced process to settle payment disputes,” the lawmakers told administration officials in the letter.

The consequences, opponents of the rule argue, would be a process that favors insurers over doctors, and pushes prices too low. They also argue that it would harm networks, particularly in rural and underserved areas, because it gives insurers incentive to push down the rates they pay to in-network providers. If the in-network rates are lower, then the default rate in arbitration is also lower.

That is the argument made specifically in a lawsuit filed last month against the Biden administration by the Texas Medical Association.

The suit alleges that in a handful of states that already have a similar strategy, such as California, a recent study shows payment rates are driven down. Citing that data and a survey by the California Medical Association, the suit says insurers now have an incentive to end contracts with better-paid in-network providers or force them to accept lower rates, since out-of-network providers then become subject to the same lower baseline.

Jack Hoadley, of Georgetown University’s Health Policy Institute, said the results could run either way, depending on whether insurers or providers are more powerful in a specific market.

“You’ve got some markets where you have a dominant insurer, and they can say to providers: ‘Take it or leave it. Because we represent most of the insurance business, we represent most patients,’” Hoadley said.

But in other places, there might be a provider group that is stronger. “All the anesthesiologists might be in one large practice in a market, and they can basically say to the insurers in that market, ‘Take it or leave it,’” he said.

In releasing the rule, the Centers for Medicare & Medicaid Services pointed to an analysis from the Congressional Budget Office that the No Surprises Act would lower premiums by about 1% and shave $17 billion off the federal deficit.

Lower premiums are an especially important goal for the administration and some of its allies, like patient advocacy groups and labor unions.

Whether networks of providers will be diminished remains an open question, Hoadley said. Surveys cited in the Texas lawsuit also show that the use of in-network services rose in some of the states with benchmarks similar to the national law, though it’s unknown whether more doctors joined networks or more people shifted to in-network providers.

It’s also unclear whether the administration will consider the lawmakers’ concerns. Some Hill staffers involved in the pushback thought the process was probably too far along to be changed and would have to be resolved in the courts. Others saw a chance for a last-minute shift.

One House staffer noted that more than 70 Democrats complaining to a Democratic White House could have an impact.

“Combined with the whole craziness of the surprise-billing battle over the past few years and the legal threat, I think there’s plenty of ballgame left,” the staffer said.

The number and complexity of school quarantine policies have left many parents with the impression there is little rhyme or reason in quarantining one kid and not a classmate.

This article was published on Tuesday, November 16, 2021 in Kaiser Health News.

At this point in the pandemic, most parents are familiar with “covid notification” letters. But the letters’ instruction on whether your kid must quarantine or not varies wildly from school to school.

In Minneapolis, students exposed to covid-19 at school are supposed to quarantine for 10 days. In the suburban Anoka-Hennepin school district, a single exposure does not trigger contact tracing or quarantining.

In Andover, Kansas, schools follow quarantine protocols set by county health departments. With students from different counties attending the same school, those sitting next to each other in classrooms could be quarantined based on two sets of rules.

In Anchorage and many schools in Texas, close contacts of classmates who test positive for covid are given the option to stay in class or to quarantine. In suburban Chicago, siblings of students with any symptom of covid are required to quarantine until their sibling tests negative.

The number and complexity of school quarantine policies — in Fort Mill, South Carolina, eight pages of guidance directs students when to quarantine — have left many parents with the impression there is little rhyme or reason in quarantining one kid and not a classmate. Sometimes rules seem to vary within families: Christina Kennedy, a teacher in Bend, Oregon, got a call when her son was exposed to a positive case in August, and he was required to quarantine. But when her daughter was a close contact to a positive case, no call ever came.

“Unfortunately, we have a natural experiment going on across the country when it comes to schools reopening, particularly regarding quarantining,” said Dr. Leana Wen, a public health professor at George Washington University. “Some of it is understandable, but there is a piecemeal approach for certain when it comes to various approaches.”

The Centers for Disease Control and Prevention’s guidance calls for unvaccinated kids exposed to someone who tests positive for covid to quarantine for a length of time determined locally. But a state or county or school district’s decision to impose a quarantine requirement is haphazard. An informal coalition that advocates for in-person learning, Ed300, found that 31 states are not automatically quarantining students from close-contact exposures.

“What we have learned from this pandemic is that when there is not a directive, school districts will behave autonomously and you’ll get this kind of outcome — good, bad or otherwise,” said David Law, superintendent of Minnesota’s Anoka-Hennepin School District.

Schools in his state act independently, Law noted.

That’s true in many other areas too. “Principals and county health officials have a lot of leeway,” said Leslie Bienen, a parent involved with Ed300 and a faculty member at the Oregon Health & Science University-Portland State University School of Public Health.

“The quarantine could be seven or 14 days,” Bienen said, and local officials have a lot of say in determining who qualifies as a close contact — defined by the CDC as having been within 6 feet of someone for a cumulative total of at least 15 minutes over a 24-hour period. But the agency has also recommended that schools maintain at least 3 feet of distance between students.

Local control isn’t necessarily a bad thing — schools should be the ones setting their rules, Wen said — but that’s why things can look so different from one school to the next, no matter how close they are in proximity.

Kennedy, the Bend, Oregon, teacher, works at a private school while her husband teaches at a public school her kids attend.

“The private school is much more prone to shutting down entire classrooms than the public school,” Kennedy said. “I know of three entire classrooms shut down since September at my private school” while zero have been shuttered in the public system.

Districts in the same county, under the purview of the same public health officials, are handling it differently, she pointed out. “Nothing is consistent. They say it’s all based on science, but we’re not allowed to question or point out anything. Why is it this way here and this way there? It’s super frustrating as a parent and as a teacher,” Kennedy said.

Another frequent complaint: Policies differ depending on whether students are there for school or for after-school activities or whether it is a community or sporting event. “What really irritates our community is that you can show up for a community event at the school or spend four hours at a sporting event and no one gets quarantined, but you can sit next to someone for 40 minutes during the school day and be out of school for 10 days,” Law said.

The confusion has left many parents wondering whether policymakers have done their homework.

Jessica Butler Bell, vice president of communications for Webster Elementary’s PTA in California’s Santa Monica-Malibu Unified School District, said parents are asking, “Are we really following the science? Or are we being too careful? It has to be rooted in logic, and I think people are going, ‘Have you thought this through?’”

Bienen co-authored an opinion piece in The Wall Street Journal titled “It’s Madness to Quarantine Schoolchildren,” citing research showing that only a small percentage of students quarantined ended up testing positive for covid as a result of the school-based contact. The group also says data from Portland Public Schools shows that students who attend Title I schools — those that receive special federal funding because they serve large numbers of low-income families — are more likely to be quarantined.

“Kids with means go on vacation or to their grandparents when they’re quarantined,” Kennedy noted. “That’s great for them, but what about kids who don’t have parents at home? They’re sitting at home with no learning, no food, no services. It exacerbates the inequities.”

But parents get equally upset when rules are lacking: Wen said she’s heard of parents doing their own informal contact tracing when they think their schools aren’t doing a thorough job.

The complicated policies have other repercussions. Some parents grow reluctant to test their kids, Kennedy said, for fear that a positive test will force them out of school or activities. And at some schools, she added, teachers delay giving out seating charts to school nurses or other public health officials for contact tracing, knowing that kids may have to quarantine after the information is shared.

Some schools are piloting a possible solution: replacing quarantines with a “test-to-stay” policy. Under such a policy, any student deemed a close contact would be able to take a rapid test and show a negative result to stay in school and avoid quarantine.

CDC Director Rochelle Walensky recently noted that “we are working with states to evaluate a test-to-stay policy as a promising potential new strategy for schools. And we anticipate that there will be guidance forthcoming.”

Wen said she is optimistic the policy could help. “It’s a way to prevent kids from being out of school.”

In Santa Monica-Malibu, one frustration Butler Bell hears from parents is that there’s no plan for ending quarantines and other layers of protection.

Parents often feel their concerns are not being considered, Kennedy said. “If [decision-makers] spent one hour inside an actual classroom, they would make different decisions,” she said.

The reason so few Missouri dentists accept Medicaid is simple, according to Vicki Wilbers, executive director of the Missouri Dental Association: The state's program pays dentists extremely poorly compared with private insurance or what a dentist could charge a patient paying cash.

This article was published on Tuesday, November 16, 2021 in Kaiser Health News.

At the Access Family Care clinics in southwestern Missouri, the next available nonemergency dental appointment is next summer. Northwest Health Services, headquartered in St. Joseph, is booked through May. The wait is a little shorter at CareSTL Health in St. Louis — around six weeks.

Roughly 275,000 Missourians are newly eligible this year for Medicaid, the federal-state public health insurance program for people with low incomes, and they can be covered for dental care, too. Missouri voters approved expansion of the program in 2020, the latest of 39 states to do so as part of the Affordable Care Act, but politics delayed its implementation until Oct. 1. Adults earning up to 138% of the federal poverty level — about $17,774 per year for an individual or $24,040 for a family of two — can now get coverage.

But one big question remains: Who will treat these newly insured dental patients?

Only 27% of dentists in Missouri accept Medicaid, according to state data, one of the lowest rates in the country. Many of them work at what are known as safety-net clinics, such as Access Family Care, Northwest Health Services and CareSTL Health. Such clinics receive federal funds to serve uninsured patients on a sliding scale and was experiencing huge demand for dental services before expansion.

The reason so few Missouri dentists accept Medicaid is simple, according to Vicki Wilbers, executive director of the Missouri Dental Association: The state’s program pays dentists extremely poorly compared with private insurance or what a dentist could charge a patient paying cash. Adding to the strain, said Wilbers, dentists who do accept Medicaid often must deal with the state plus private insurers that administer Medicaid through a program known as managed care.

“You have more people on the rolls, you still don’t have reimbursement rates increase,” Wilbers said. “And it’s cumbersome.”

Still, for these new patients, the coverage can be life-changing.

Only 37% of adults in the state with incomes under $15,000 per year saw a dentist in 2018 compared with 76% of adults earning over $50,000, according to a state report. A survey by the American Dental Association found 53% of low-income Missourians have difficulty chewing, 43% avoid smiling because of the condition of their mouth and 40% experience pain.

“I just don’t think those stories are told enough,” said Steve Douglas, spokesperson for Access Family Care in Neosho.

Douglas described a patient of the clinic who believes his so-far-unsuccessful quest for higher-paying work has been hindered by the appearance of his teeth.

“We’re hoping that with the Medicaid expansion we can get him in for some care,” Douglas said. “He would like to save some of his teeth and not go to full dentures.”

About 62% of Missouri adults making under $15,000 per year have lost at least one tooth to decay or gum disease, and 42% of people 65 and older in that income range have lost all of them, according to the state report. For Missourians earning over $50,000, those rates are 34% and 8%, respectively.

Part of the dental care backlog at Access Family Care, which offers dental services at five locations around southwestern Missouri, is due to the pandemic. The clinic laid off all 95 of its dental staffers in March 2020 before gradually building back to full capacity. As with dental practices nationwide, many of their patients are now coming to get the dental work done that they delayed earlier over fears of exposure to the coronavirus.

But central to the huge demand is an overall need for more providers. Nearly 1.7 million Missourians live in a federally designated dental professional shortage area, one of the highest levels of unmet needs in the country. It’d take another 365 dentists to fill that void, at least one extra dentist for every 10 already practicing in the state.

“We could easily employ another four dentists and still have high demand,” Douglas said.

His clinic, Access Family Care, has indeed hired two new dentists to start in 2022. To manage the dental caseload until then, though, it had to temporarily stop seeing new patients.

In St. Louis, Dr. Elena Ignatova, director of dental services at CareSTL Health, had 18 patients scheduled on a recent Wednesday in November. About a quarter of them were insured through Medicaid.

By 10 a.m., she had cast a mold of one patient’s mouth to fit dentures, referred another to an oral surgeon for a root canal and prepped a fourth-year dental student for the extraction of a Medicaid patient’s remaining teeth. In Missouri, Medicaid covers simple tooth extractions for adults but not root canals or crowns.

“We remove teeth because the other treatment is too expensive and they cannot afford it,” Ignatova said. “Then it can take years for those patients to come up with the money for dentures.”

Ignatova is booked into February, but the clinic still takes walk-ins for dental emergencies. She’s also working her way through a waiting list of 39 patients who might be able to show up quickly if a cancellation or no-show opens a spot in her schedule.

There is easily enough demand for another dentist, but Ignatova said they’re still working on hiring the dental assistants and hygienists needed to reopen the school-based clinics for kids they operated before the pandemic. Those hirings are in the works, but it is slow going. As with many health care facilities, she and others said, President Joe Biden’s vaccine mandates have added an extra hurdle to recruiting and retaining staff.

One clinic that isn’t seeing a bottleneck of dental patients, though, is KC Care Health Center in Kansas City. Kristine Cody, the clinic’s vice president of oral health services, said a new patient could be seen there in about a week. The Kansas City region benefits from having the University of Missouri-Kansas City School of Dentistry, which offers reduced-cost care to patients at the clinic where its students are trained, plus several other safety-net clinics.

KC Care also added two dentists and extended its clinical hours in anticipation of Medicaid expansion.

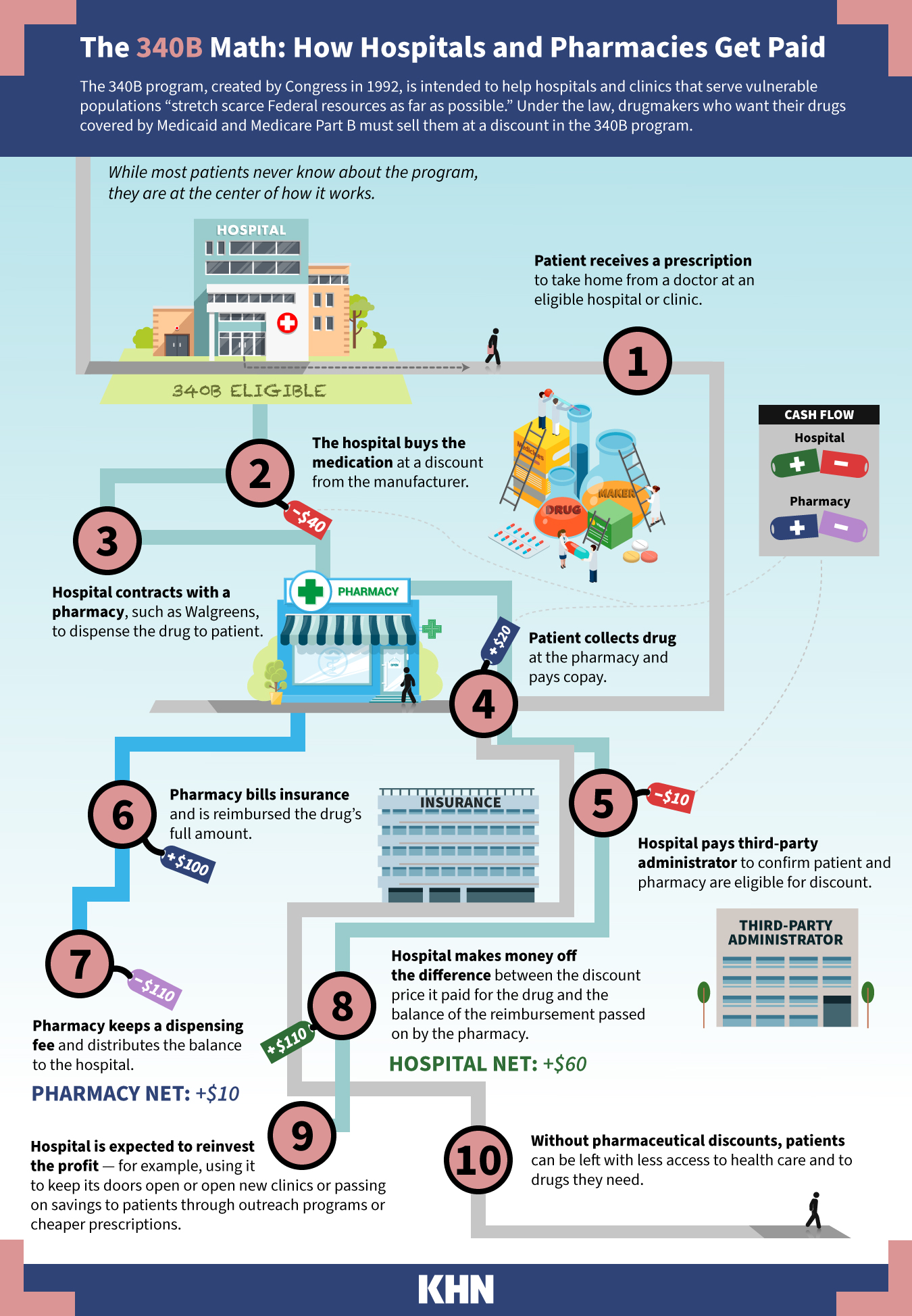

Congress created the 340B program in 1992 to provide extra funding for hospitals and clinics, especially those serving the poor and elderly, but the law does not require patients to benefit directly, a nuance that has fueled great conflict about how the program works and should be regulated.

This article was published on Tuesday, November 16, 2021 in Kaiser Health News.

In early July, as the covid-19 pandemic slammed rural America, the president of a small Kansas hospital sat down on a Friday afternoon and wrote the president of the United States to plead for help.

“I do not intend to add to your burden,” said Brian Williams, a retired Army lieutenant colonel and Desert Storm combat veteran. He said his hospital, Labette Health, was “like a war zone,” inundated with unvaccinated patients. A department head had threatened to resign, saying he could not “watch one more body be carried out.”

But Williams wasn’t seeking pandemic relief.

Instead, he asked President Joe Biden to confront pharmaceutical manufacturers Eli Lilly and Co., Novo Nordisk and others for refusing to honor a federal drug discount program for hospitals and clinics. The program gives Williams millions to pay staff members, ensure remote clinics remain open and provide charity care for patients unable to pay, he said.

“During a global pandemic, I think health care workers deserve a little bit more respect than to have resources taken away,” Williams said in an interview with KHN and InvestigateTV. “Every one of those [drug] companies, I looked them up, and they were not suffering tremendous [financial] losses, as hospitals were.”

Eli Lilly’s stock price increased nearly 40% and the company’s value rose by $59 billion in the first seven months of 2021. In the same period, Labette Health lost $1.2 million in revenue just from the missed savings on prescriptions, Williams said.

Lilly and other manufacturers, though, are holding their ground. They refuse to offer discounts to thousands of hospital-contracted pharmacies, saying the program has grown beyond its intended use and lacks federal checks and balances against duplicate discounts and other abuses. In lawsuits, they contend the billions in discounted sales they provide are rarely passed on to patients and instead are swallowed up by middlemen like contract pharmacies and third-party administrators.

Congress created the so-called 340B program in 1992 to provide extra funding for hospitals and clinics, especially those serving the poor and elderly. The purpose, lawmakers wrote, is to “stretch scarce Federal resources as far as possible, reaching more eligible patients and providing more comprehensive services.”

Companies that want their drugs covered by Medicaid or Medicare Part B are required to offer 340B discounts, typically 25% to 50% off what they might otherwise pay. Hospitals and clinics buy the drugs at the discount and then are reimbursed by an insurance company, Medicare or Medicaid at the higher negotiated rate. The difference is kept by the hospital or clinic to use as it sees fit.

The law does not require patients to benefit directly, a nuance that has fueled great conflict about how the program works and should be regulated.

Hannah Norman/KHN; Getty Images

The 340B program’s reach exploded after federal regulators ruled in 2010 that hospitals and clinics could contract with an unlimited number of retail pharmacies such as Walgreens and CVS, which are paid a fee to dispense the discounted drugs. The growth, coupled with long-held questions about regulatory authority, puts the program at a tipping point, with patients stuck in the middle, industry experts say.

The number of pharmacies contracted to work with 340B hospitals to dispense the discounted drugs has soared. It’s reached more than 31,000 nationwide this year from just over 1,700 in 2010, according to an analysis of federal data by InvestigateTV and KHN.

One eye-popping statistic: The drugs purchased under 340B climbed to $38 billion in 2020 from $5.3 billion in 2010, according to the Health Resources and Services Administration, or HRSA, which oversees the program.

Interests on both sides of the program — hospitals and drugmakers — say they are at the mercy of a program designed with the best of intentions, now run amok, hijacked by for-profit companies and wealthy hospitals trying to profit from its largesse.

Adam J. Fein, chief executive of the industry research organization Drug Channels Institute, estimates that nearly half the nation’s retail, mail and specialty pharmacies now profit from 340B: The program, he said, is “essentially taking over the pharmacy industry.”

Legal fights about the program have landed before the U.S. Supreme Court, which is slated to hear arguments this month in American Hospital Association v. Becerra. The hospital industry is challenging a 2018 rule by the Trump administration to cut reimbursement on certain 340B drugs by 28.5%. As Biden’s HHS secretary, Xavier Becerra has upheld the rule.

Most important, the administration says, is to make sure providers use the savings to benefit patients. In an interview with KHN and InvestigateTV, Rear Adm. Krista Pedley, director of the Office of Special Health Initiatives, which oversees the program within Becerra’s agency, said, “We need legislative changes to help make that happen and require that.”

'Deeply Troubling'

When Sen. Joe Manchin (D-W.Va.) asked during a June appropriations hearing about pharmaceutical companies denying the discounts, Becerra said the drugmakers are violating the law.

“I hope what you’ll do is give us more authority” to regulate the program, Becerra said.

Manchin responded: “I really think we could do that in a bipartisan way, because I’ll tell ya, we’re all being affected.”

As California’s attorney general, Becerra led a coalition of national lawmakers calling for the federal government to hold the manufacturers accountable for their “deeply troubling” actions to undermine the program. At HHS, Becerra put the companies on notice.

Drugmakers — Lilly, AstraZeneca, Novo Nordisk, Sanofi, Novartis and United Therapeutics — took the matter to court, filing several lawsuits. This month, a federal judge ruled that the companies are not required to provide the discounts. A judge in Lilly’s case criticized the “unilateral” action by drugmakers but ruled that the U.S. government’s effort to force them to honor the discounts was invalid.

Notably, U.S. District Court Judge Sarah Evans Barker in Indianapolis wrote that manufacturers believe they are “at the mercy of a system run amok” and that the program “can no longer be held together and implemented fairly” solely through the agency’s guidance and inconsistent messaging.

Becerra requested $17 million annually for 340B program oversight, a $7 million bump. The money would establish a dispute review panel and increase the audits the agency does on manufacturers as well as the providers.

Williams — at his small hospital in rural Parsons, Kansas — said the nearly $4.3 million the hospital gains each year from 340B has allowed him to add a full-time position for case management, increase staffing hours, develop after-school programs and open clinics in impoverished towns that lacked health care.

The hospital has about 20 pharmacies under active contracts, according to the federal database. Williams said it includes locally owned shops like Bowen Pharmacy as well as corporate giants like Walgreens and Walmart, sites that are convenient for patients. A pharmacy added in 2019 is in Frisco, Texas — a mail-order facility that ships specialty drugs directly to patients’ homes.

Patients, Williams said, directly benefit from the federal program: “I’d love to have the CEO of Eli Lilly come here and I’ll take him around and I’ll show him a town of 1,200 where 40% of the population live below the poverty level.”

“Some of our patients come there on a bicycle or in a wheelchair,” Williams said. “I can go 30 minutes in any direction and find pretty tough people living in pretty … pretty austere circumstances.”

One Hospital, 300 Pharmacies

Vanderbilt University Medical Center, based in Nashville, has added three regional hospitals, clinics and providers in recent years — growth that has fueled its rise in contract pharmacies from zero in 2010 to 300 this year. The pharmacies, which reach across Tennessee and all the way to California, “in each instance serve VUMC patients,” Vanderbilt spokesperson John Howser said.

Financial filings do not disclose how much Vanderbilt gains annually from the 340B program, and Howser declined to disclose the amount. The medical system’s operating revenue grew $649 million, or 13%, to $5.5 billion in fiscal year 2021 compared with 2020, according to its latest financial disclosure. Its operating profit rose 25% to $177 million in 2021 compared with 2020.

According to an amicus brief filed in March for the American Hospital Association v. Becerra case, Vanderbilt spends more than $500 million annually on community benefits, such as charity care. Revenue from the 340B program supports low-income programs including medication assistance, home infusion medications and a pharmacy program at a health clinic run by students.

In the brief, Vanderbilt states the government’s cut in Medicare reimbursement has cost the system $12.4 million in 340B savings and will “impact VUMC’s ability to continue to fund community benefit programs at historic levels.”

Large regional health systems have been particularly active in expanding their contract pharmacy networks. The top three — University of Michigan Hospitals and Health Centers, Cambridge Public Health Commission in Massachusetts and Henry Ford Hospital in Detroit — had zero contracts with outside pharmacies in 2010, and each now has more than 500.

InvestigateTV and KHN contacted the 10 providers with the most contract pharmacies and asked why they saw such growth, how much revenue 340B generates and how the money was used.

While some said the money went for charity care and community programs, others did not respond.

Why not require hospitals to report precisely how they use the savings to benefit patients?

It would be “burdensome,” said Maureen Testoni, chief executive of 340B Health, which represents health systems.

She said her organization does not support mandating new reporting for nonprofit hospitals, which are required to submit annual cost reports and tax filings. The advocacy group has funded research that shows the savings from discounts go to patients. Hospitals enrolled in the program are much more likely to provide free care and specialty services, such as transportation, that are “typically not the ones you can use to pad your pockets,” she said.

Testoni said program growth is good because it means more care can be provided in outpatient settings and by safety-net providers for low-income populations. The bigger sales numbers, she said, could stem from more prescriptions or from higher drug prices. Detailed information about either metric is not public.

“Are we concerned that somehow pharmaceutical companies are being hurt by this?” Testoni said. “Because I’ve never seen any evidence of that in terms of their revenue going down or them having trouble keeping their doors open.”

'Essentially Taking Over'

Hospitals aren’t required to prove that the large pharmacy networks serve uninsured or needy patients. The larger networks enrich the hospitals and the pharmacies, said Fein of Drug Channels.

A 2018 Government Accountability Office report found that a hospital or clinic generally pays a flat dispensing fee — typically from $6 to $15 — for each eligible prescription a pharmacy processed. And pharmacies can contract with multiple health care providers: One Walmart central fill facility in Spring, Texas, contracted with 1,842 340B hospitals and clinics, the InvestigateTV and KHN analysis found.

Recent securities filings for Walmart, Walgreens and CVS Health — the biggest players in the contract pharmacy market —- do not provide line-item detail on how many 340B prescriptions are processed or the revenue those transactions generate. Walmart did not respond to requests for comment. CVS declined to comment.

CVS reported in an August financial filing that operating income increased by a third between March and June compared with a year ago and noted that 340B business contributed to that increase but provided no further detail. The company acquired 340B contract pharmacy administrator Wellpartner in 2017.

Walgreens mentioned the program in its 2020 annual financial filing, noting that changes to government pricing and regulations “could also significantly reduce our profitability.” Walgreens spokesperson Rebekah Pajak said that many of the company’s stores are in underserved areas and that it is proud to help fulfill the program’s goals. She declined to disclose the dispensing fees or terms of its contracts with hospitals and clinics.

Karyn Schwartz, vice president of policy and research at PhRMA, called the 340B program a “black box” and said drug companies would like more transparency because they “really have no way of knowing” how hospitals and pharmacies use their discounts.

Drugmakers said they continue to participate in the program by sending direct discounts to the hospitals but have eliminated some or all of the discounts passed through contract pharmacies because they didn’t trust the transactions, according to emails the companies sent to KHN and InvestigateTV. Novartis, which announced last year that it would sell drugs at a discount only for pharmacies within 40 miles of a hospital, said there is a “complete absence of transparency” in the contracts between hospitals and pharmacies.

“Contract pharmacy arrangements benefit for-profit pharmacies, third-party administrators, other middlemen and hospitals,” Novartis spokesperson Caryn Marshall wrote in an email.

“Lilly welcomes reforms where patients are identified as 340B eligible at the point-of-sale and share in discounts under the program,” said Tarsis Lopez, Eli Lilly spokesperson.

Getting By on 'Half a Dose'

Meanwhile, as businesses wage war over profits, patients are stuck. Andrew Kosowski, a 75-year-old retired police officer with diabetes, was shocked last year when he lost access to discounted drugs from 340B.

Kosowski is a patient at UnityPoint Health in Peoria, Illinois, which uses funds from the program to supplement the prescription costs of low-income and Medicare patients. Under 340B, many of his prescriptions were $15 each.

Without the discount, Kosowski’s insulin and other drugs had cost more each month than his Social Security check delivered. “I wasn’t going to spend that kind of money,” he said. He took “half a dose to get me by.”

He recalled how his feet hurt and his mind was affected without his full prescriptions.

PhRMA’s Schwartz declined to speak to Kosowski’s crisis but said the industry participates in 340B and would like to see direct patient benefit. “We hope policymakers step in and really clarify the role that for-profit pharmacies are supposed to be playing in this program and ensure that patients benefit,” Schwartz said.

Kosowski was fortunate to have an ally in Anne Webster, a nurse practitioner at UnityPoint who guided him through months of filling out forms to eventually qualify for financial assistance directly from Novo Nordisk.

The assistance, though, does not cover medications from other companies that he had gotten at the 340B discount price — medications that had helped him better manage his diabetes.

Webster said pharma’s standoff came at the worst possible time: “A Type 2 diabetic is so high-risk for mortality from coronavirus. And they require more insulin if they are ill with the virus.”

Kosowski is not her only patient missing prescriptions.

“I think I prescribed over 2,000 prescriptions in one year to the 340B program for my patients who are underinsured, not insured and are financially challenged,” Webster said.

KHN data editor Holly Hacker contributed to this report.

A California law signed by Gov. Gavin Newsom last month may help you sort through a tangle of medical bills to figure out what your health plan will cover and when the coverage kicks in.

This article was published on Monday, November 15, 2021 in Kaiser Health News.

If you’ve ever had a serious illness or cared for someone who has, you know how quickly the medical bills can pile up: from labs, radiology clinics, pharmacies, doctors, different departments within the same hospital — some of them in your insurance network, others not.

It can be extremely confusing, no matter how clever you are, to determine which bills you need to pay. If you’re sick, or have technological, cultural or language barriers — not to mention financial difficulties — navigating this maze can be especially intimidating.

A California law signed by Gov. Gavin Newsom last month may help you sort through a tangle of medical bills to figure out what your health plan will cover and when the coverage kicks in.

The law, SB 368, requires most state-regulated private-sector health plans to send enrollees updates, for every month in which they received care, showing how much they have paid toward their annual deductible — the amount a person must shell out before insurance begins to cover most of their care — and how close they are to reaching out-of-pocket limits, the amount after which the insurer pays for 100% of care.

The law, which takes effect in July, should help people with costly chronic conditions who need to keep better track of how much they owe, and healthy ones who rarely seek care but might suddenly encounter unexpected medical circumstances.

“It’s not that hard to hit those maximums, and it doesn’t take a cancer diagnosis to get there,” says Dylan Roby, a professor of public health at the University of California-Irvine. “It could be one ER visit with a procedure. A broken leg could get you there pretty easily.”

The new law requires health plans to send out-of-pocket updates via mail unless the insured opts for electronic delivery. The information must also be stored in a format that is accessible to customers at any time.

SB 368 “is part of a larger need to provide transparency about individuals’ out-of-pocket risks,” says Roby.

Consumers often are unaware, he notes, of what’s available for free under the Affordable Care Act, including preventive services like screening tests and immunizations. Most health plans offered through Covered California, the state’s ACA marketplace, also must cover outpatient services, including imaging, specialist appointments and physical therapy, before the deductible is met.

One potential pitfall of the new law, Roby observes, is that insurers can crunch numbers based only on the claims they’ve processed, and some doctors and other providers might take six months or more to file claims. That means the information plans send to enrollees could be outdated.

At present, state law imposes no specific requirement on insurers to inform enrollees of their current financial liabilities, but some plans already do so — either in the “explanation of benefits” they send after care is received, or in response to a customer request.

“This law makes an optional practice a requirement,” says state Sen. Monique Limón (D-Santa Barbara), who authored the legislation. “And it’s a good practice.”

The new law should be helpful to a growing number of people, given the increasing prevalence of health plans with ever-larger deductibles.

Between 2012 and 2020, the percentage of California workers with single coverage who had an annual deductible of $1,000 or greater quadrupled, to 54%. And among families enrolled in health plans with deductibles, 70% had deductibles of $2,000 or higher last year, compared with 31% eight years earlier.

For the cheapest Covered California plans, the deductible this year is $6,300 for an individual and $12,600 for a family. And there’s a separate deductible for prescription drugs (the new law requires health plans to inform enrollees where they stand on all their deductibles).

As deductibles rise, health plan members are seeing the financial protection of their insurance kick in later and later in the year. And in many cases, after meeting their deductibles they still need to spend a thousand or more before reaching out-of-pocket spending limits for the year.

People with serious diagnoses such as cancer, HIV, multiple sclerosis or cystic fibrosis frequently make such calculations.

Stacey Armato, a 41-year-old mother of three in Hermosa Beach, California, has a 6-year-old son with cystic fibrosis, a serious progressive lung disease. Her son, Massimo, takes about a dozen medications, with costs well into the thousands of dollars each month.

Armato and her family are luckier than many: They have good insurance that limits their total spending on Massimo’s care to about $6,000 a year. But that is still enough to make them rethink spending plans at times. “I’m always going to prioritize my son’s care,” Armato says.

She likes the new law. “I think transparency about how much a patient is spending and what their financial obligations are is really important,” she says.

Some families coping with cystic fibrosis and other expensive illnesses face much starker trade-offs — choosing between treatment and paying their rent, for example. In those cases, it can be indispensable to know when the financial hemorrhaging will stop, easing pressure on the family budget.

The new law can also be useful if you, like many people, postponed an elective surgery because of the pandemic — a hip replacement or cataract removal, for example — and want to reschedule it now. The best timing, financially speaking, will be when you are close to reaching your deductible and out-of-pocket spending limit — or if you already have reached them. If you know where you stand, you can schedule the procedure for a time when your financial liability will be minimal.

The law might also help people avoid paying money they don’t actually owe. “Sometimes when people see any kind of bill, they think they need to pay it,” says Jen Flory, a policy advocate at the Western Center on Law & Poverty, which supported the legislation. “So unless they understand that, ‘Oh, I reached my deductible, or my out-of-pocket max,’ people panic and do whatever they need to do to pay the bill. And it can be hard to get the money back from providers if they pay unnecessarily.”

Although your insurer is not required to provide your out-of-pocket status until the law takes effect in July, you can still call the customer help line and ask for it — or for clarification about a bill. If you don’t get the answer you want, ask your health plan to tell you who regulates it, and call that agency. It would usually be the Department of Managed Health Care, at 888-466-2219 or HealthHelp.ca.gov, or the California Department of Insurance, reachable at 800-927-4357.

If you need help sorting through heaps of medical bills, you could hire a professional patient advocate, who will typically charge you a percentage of the amount they save you. To find patient advocates in your area, log on to www.advoconnection.com

To see if you qualify for free assistance, try the Patient Advocate Foundation (www.patientadvocate.org or 800-532-5274), which helps people resolve unaffordable health bills and also provides disease-specific, need-based financial aid.

Independent pharmacies are struggling due to the vertical integration among drugstore chains, insurance companies and pharmaceutical benefit managers, which gives those companies market power that community drugstores can’t match.

This article was published on Monday, November 15, 2021 in Kaiser Health News.

Batson’s Drug Store seems like a throwback to a simpler time. The independently owned pharmacy in Howard, Kansas, still runs an old-fashioned soda counter and hand-dips ice cream. But the drugstore, the only one in the entire county, teeters on the edge between nostalgia and extinction.

Julie Perkins, pharmacist and owner of Batson’s, graduated from the local high school and returned after pharmacy school to buy the drugstore more than two decades ago. She and her husband bought the grocery store next door in 2006 to help diversify revenue and put the pharmacy on firmer footing.

But with the pandemic exacerbating the competitive pressures from large retail chains, which can operate at lower prices, and from pharmaceutical intermediaries, which can impose high fees retroactively, Perkins wonders how long her business can remain viable.

She worries about what will happen to her customers if she can’t keep the pharmacy running. Elk County, with a population of 2,500, has no hospital and only a couple of doctors, so residents must travel more than an hour to Wichita for anything beyond primary care.

“That’s why I hang on,” Perkins said. “These people have relied on the store from way before I was even here.”

Corner pharmacies, once widespread in large cities and rural hamlets alike, are disappearing from many areas of the country, leaving an estimated 41 million Americans in what are known as drugstore deserts, without easy access to pharmacies. An analysis by GoodRx, an online drug price comparison tool, found that 12% of Americans have to drive more than 15 minutes to reach the closest pharmacy or don’t have enough pharmacies nearby to meet demand. That includes majorities of people in more than 40% of counties.

Independent pharmacies are struggling due to the vertical integration among drugstore chains, insurance companies and pharmaceutical benefit managers, which gives those companies market power that community drugstores can’t match.

Insurers also have ratcheted down what they will pay for prescription drugs, squeezing margins to levels that pharmacists call unsustainable. As the insurers’ drug plans steered patients to their affiliated drugstores, independent shops watched their customers drift away. They find themselves at the mercy of pharmaceutical intermediaries, which claw back pharmacy revenue through retroactive fees and aggressive audits, leaving local pharmacists unsure if they’ll end the year in the black.

That has a direct impact on customers, particularly older ones, who face higher copays for prescription medications if they have a drug plan, and higher list prices if they don’t. If their local pharmacy can’t survive, they may be forced to travel long distances to the nearest drugstore or endure waits to get their prescriptions from understaffed pharmacies serving more and more patients.

“Living in an area with low pharmacy density could increase wait times, decrease supply, and make it harder to shop around for prescription medications,” said Tori Marsh, GoodRx’s lead researcher on the drugstore desert study.

The financial pressures on independent drugstores began mounting two decades ago when Medicare instituted its Part D program using private insurance plans: Pharmacies’ most frequent customers went from paying cash for list prices to using insurance coverage that paid lower negotiated rates.

“A market clearance occurred, a big bolus of pharmacy closures,” said Keith Mueller, director of the Rural Policy Research Institute.

Independent pharmacies saw their margins shrink. On average, a pharmacy’s cost of dispensing a single prescription, factoring in labor, rent, utilities and other overhead, ranges from $9 to $15. But the reimbursement is often far less.

Multiple pharmacists said that about half of drug plan reimbursements fail to cover the costs of drugs and their overhead.

“What you’re left with is that 50% of claims that you can make some money on, and really, the tiny percentage of claims where you make an extremely high amount of money,” said Nate Hux, who owns an independent pharmacy in Pickerington, Ohio.

It’s that tiny sliver of wildly overpaid drugs, especially generics, that determines whether a pharmacy can survive. A generic drug that costs $4 might get reimbursed by a drug plan at $4,000.

“Filling a generic prescription, from a financial standpoint, is like pulling the slots at a casino,” said Ben Jolley, an independent pharmacist in Salt Lake City. “Sometimes you lose a quarter, sometimes you lose a buck, and sometimes you make $500. But you have to have those prescriptions that you make $500 on to make up for the losses on the rest of your meds.”

Some pharmacies increase their list prices to ensure they capture the highest reimbursements that drug plans are willing to pay. But that raises prices for patients paying cash.

Jolley, who also works as a consultant for pharmacies across the country, said some pharmacists game the system by billing excessive charges for drugs they mix on-site or calling physicians to switch patients to more profitable drugs.

“Pharmacies that play this game get exceptionally wealthy,” he said. “Most pharmacies either don’t feel comfortable playing this game or aren’t aware that that’s how the system works, so they get left behind. That’s why you see all these pharmacies closing.”

Pharmacy benefit managers, brokers known as PBMs, also steer customers away from independent pharmacies to affiliated chain, mail-order or specialty pharmacies with lower out-of-pockets costs. Some PBMs prevent local pharmacies from offering the most expensive drugs at all.

The benefit managers counter that there are more independent pharmacies today than there were 10 years ago. An analysis conducted on behalf of the Pharmaceutical Care Management Association, a trade group that represents pharmacy benefit managers, showed a 13% increase in the number of independently owned pharmacies from 2010 to 2019. However, many of those new stores opened in communities that already had pharmacies.

“PBMs are not seeking to put independent pharmacies out of business,” said Greg Lopes, a spokesperson for the trade group. “PBMs are trying and often succeeding in lowering drug costs.”

The insurers’ trade group, AHIP, formerly America’s Health Insurance Plans, declined to comment.

Katie Koziara, a spokesperson for the Pharmaceutical Research and Manufacturers of America, an industry group representing drugmakers, said the large market power of PBMs can leave patients with fewer choices.

“The system might work well for health plans and these middlemen, but it creates difficult access barriers for vulnerable patients,” Koziara said. “We’re concerned about the emerging issue of ‘pharmacy deserts’ where patients, particularly among communities of color, cannot readily access a community pharmacy for their medications.”

Independent pharmacists routinely identify those middle-manager companies as the leading cause of their troubles. At Batson’s drugstore in rural Kansas, Perkins recently had a customer who had been taking Emgality, an injectable monoclonal antibody treatment for migraines made by Eli Lilly and Co., that typically retails for up to $760 a month. But the customer’s drug plan wouldn’t pay Batson’s to fill it, forcing her to wait until it could be mailed from a specialty pharmacy.

Frustratingly, Perkins said, patients who get pushed to order drugs by mail often bring them to her when they need help deciphering how to use them.

Even when pharmacies make money on a prescription, there’s no guarantee they can keep much of the profit. Drug plans charge pharmacies fees every time they need to interact with the PBM’s claims database. While those fees average only 10 to 15 cents per transaction, a busy pharmacy might need to check the database hundreds of times a day.

PBMs also have implemented retroactive fees based on performance metrics they set. Pharmacies can wind up losing money on a prescription filled months earlier. PBMs describe these as quality measures, but pharmacists complain they are more about sales volume. Many of the metrics track how diligently patients take their medication, which pharmacies can hardly control.

One PBM’s contract, obtained by Axios, showed only 1% of pharmacies are able to avoid retroactive fees.

Jeff Olson, who owns three rural pharmacies in Iowa, said he paid $52,000 in retroactive fees on revenue of $6 million in 2015. While his annual revenue remained flat through 2020, those retroactive fees last year totaled $225,000.

“That’s money that can’t be used for payroll, that can’t be used to add those other services that your community needs,” Olson said.

Moreover, Olson said, he doesn’t know what metrics insurance plans use to evaluate his performance and calculate the fees.

“They define quality themselves,” said Ronna Hauser, vice president of pharmacy affairs for the National Community Pharmacists Association. “If you have 20 Part D plans you contract with, that’s 20 different quality programs that you’re supposed to be aware of and keep up with.”

According to the Centers for Medicare and Medicaid Services, such retroactive fees were 915 times as high in 2019 as in 2010. The resulting higher prices mean Medicare beneficiaries burn through their initial coverage period faster and enter a coverage gap, or “doughnut hole,” sooner.

At Olson’s pharmacy in St. Charles, Iowa, a town of fewer than 1,000 people, fees and other financial pressures forced Olson to scale back and operate the store as a telepharmacy. Technicians fill prescriptions under the eye of an off-site pharmacist, and customers see a pharmacist only one day a week.

For a town with no other health care provider, that means six days when no one can provide vaccinations or test for strep throat.

Back in Howard, Debbie Lane, 70, likes the personal service Perkins offers at Batson’s.