A study by the Lown Institute puts the spotlight on the value of nonprofits' community contributions.

Eighty percent of nonprofit hospitals are spending less on community support than what they're receiving in estimated tax breaks, according to a report by the Lown Institute.

The analysis by the think tank questions the value nonprofits are providing to their community while receiving tax breaks under federal, state, and local laws with the expectation that they'll pay it forward through financial aid and wellness programs.

Using 2021 IRS data for 2,425 nonprofit hospitals across the country, researchers found that more than 1,900 operators pay less than their "fair share." The combined fair share deficits of nonprofits totaled $25.7 billion, or enough to erase 29% of the country's medical debt, the report stated.

Only five states had a majority of hospitals with a fair share surplus: Delaware, Montana, Maryland, Texas, and Utah. Meanwhile, Michigan, West Virginia, Louisiana, Washington, and Rhode Island had 97% or more hospitals with a fair share deficit.

On average, hospitals spent 3.87% of their budget on charity care, but the proportion varied widely depending on the hospital.

Among the biggest offenders of skimping on community spending were Catholic health systems, which made up five of the top 10 systems with the greatest fair share deficits: Providence (-$1 billion), CommonSpirit (-$923 million), Trinity (-$784 million), Ascension (-$614 million), and Bon Secours Mercy (-$488 million).

Some of the hospitals the report highlighted for having significant fair share surpluses were Atlanta-based Grady Memorial Hospital, which had a fair share surplus for the third year in a row ($71 million), Chicago-based Mount Sinai Hospital ($67 million), and Los Angeles-based Martin Luther King Jr. Community Hospital ($14 million).

The Lown Institute also published a policy brief alongside the report to recommend changes for improving fair spending, including minimum thresholds for community spending and enforcement actions for noncompliance.

"Federal regulation of community benefit spending is woefully ineffective and in need of reform," Vikas Saini, president of the Lown Institute, said in the release. "Though hospitals are required to report their community contributions to the IRS, there is no minimum spend, there are many loopholes, and enforcement is practically nonexistent."

In response to the report, American Hospital Association president and CEO Rick Pollack released a statement saying the analysis "cherry-picks categories of community benefit and ignores other areas of great importance" and "suffers from the same biases, flaws and shortcomings as its previous reports."

The Lown Institute's findings don't fully take into account aspects like underpayments from Medicaid and Medicare, or Medicaid expansion, according to the AHA.

Nevertheless, nonprofit hospital leaders must focus on meeting charity goals to ensure the sustainability of not only their community, but of their own organization.

Michael Slubowski, president and CEO of Trinity Health, told HealthLeaders last year: "We're being very proactive in making sure that people realize that we are living out our charitable purpose, and for us being a faith-based health system, it's endemic to our mission."

Aspirus Health CEO Matt Heywood shares how to approach a potential merger.

As more health systems turn to M&A to achieve financial stability and growth, CEOs should be prepared to get the most out of a deal.

Matt Heywood, CEO of Wausau, Wisconsin-based Aspirus Health, just completed his own merger with Duluth, Minnesota-based St. Luke’s and believes hospital leaders must act with intent when bringing on a partner.

In a conversation with HealthLeaders, Heywood highlighted three key strategies fellow CEOs should utilize when taking steps towards a merger.

The Connecticut-based operator cut 60 positions to offset the costs associated with Medicare Advantage delays and denials.

Repeated Medicare Advantage (MA) claim denials left one Connecticut hospital in financial peril, causing it to significantly cut down on staff.

Bristol Hospital CEO Kurt Barwis told the Hartford Courant that in an effort to save on costs stemming from lack of reimbursement from insurers, the operator will eliminate 60 jobs, 21 of which will result in layoffs.

The MA “abuse” is the latest instance of the private program causing problems for providers, with Barwis reporting that MA insurers continue to increase their rate of denials while further delaying payments that aren’t denied.

Bristol Hospital, which operates 154 beds and physician and lab networks in 20 locations, has 63% of its Medicare patients on MA plans, while 5 to 6% of the hospital’s budget goes to insurer administrative expenses, the Courant reported.

The hospital has been facing a financial crunch in recent years and reported a $12.8 million operating loss in fiscal 2023. By slashing 60 jobs, Barwis revealed that the organization will save $6.1 million.

“We went through an extensive process to find ways to make our processes more efficient and find any opportunity to reduce positions that wouldn’t affect patient care,” Barwis told the Courant. “We don’t have a choice. All the nice-to-haves are being taken out by the lack of insurance payment and the lack of reimbursement.”

MA specifically has been criticized for delays and denials, with recent data by Kodiak Solutions finding that the value of claims taking longer than 90 days to be paid has increased by over 40% for MA plans since 2020.

“Our primary care is to take care of patients, their single focus is shareholder value and profits,” Barwis told the Courant. “The Medicare Advantage abuse is outrageous.”

Turning to termination

Many hospitals and health systems are resorting to terminating their MA contracts to counteract the financial and administrative burden of the program.

Scripps Health is one of those organizations, with two medical groups within the system ending their MA contracts for 2024 due to low payments and denials.

Chris Van Goder, president and CEO of Scripps, told USA Today that after failing to negotiate more favorable reimbursement rates, the system decided to cut loose to alleviate their $75 million in annual losses.

That strategy isn’t a viable path for every hospital, but providers may have more options than they think.

“Providers are becoming more capable in measuring the impact of the slow or rejected payments, and providers are looking at the actual cost of care by patient,” Britt Berrett, managing director and teaching professor at Brigham Young University and former CEO with HCA, Texas Health Resources, and SHARP Healthcare, told HealthLeaders. “Payers need to be aware that.”

The cyberattack is the latest event to force leaders to alter their approach.

Hospital and health systems have been going through the wringer for a few years now. The last thing CEOs needed on their plate was a cyberattack at the scale and magnitude of the one Change Healthcare suffered.

And yet, what is being called “the most significant cyberattack on the U.S. healthcare system in American history” is now the latest event in a series of twists and turns to send a shiver down hospital leaders’ spines and have them rethinking their strategies.

“Cybersecurity issues are just added icing on the cake,” Matt Heywood, CEO of Aspirus Health, told HealthLeaders.

The financial implications have been massive.

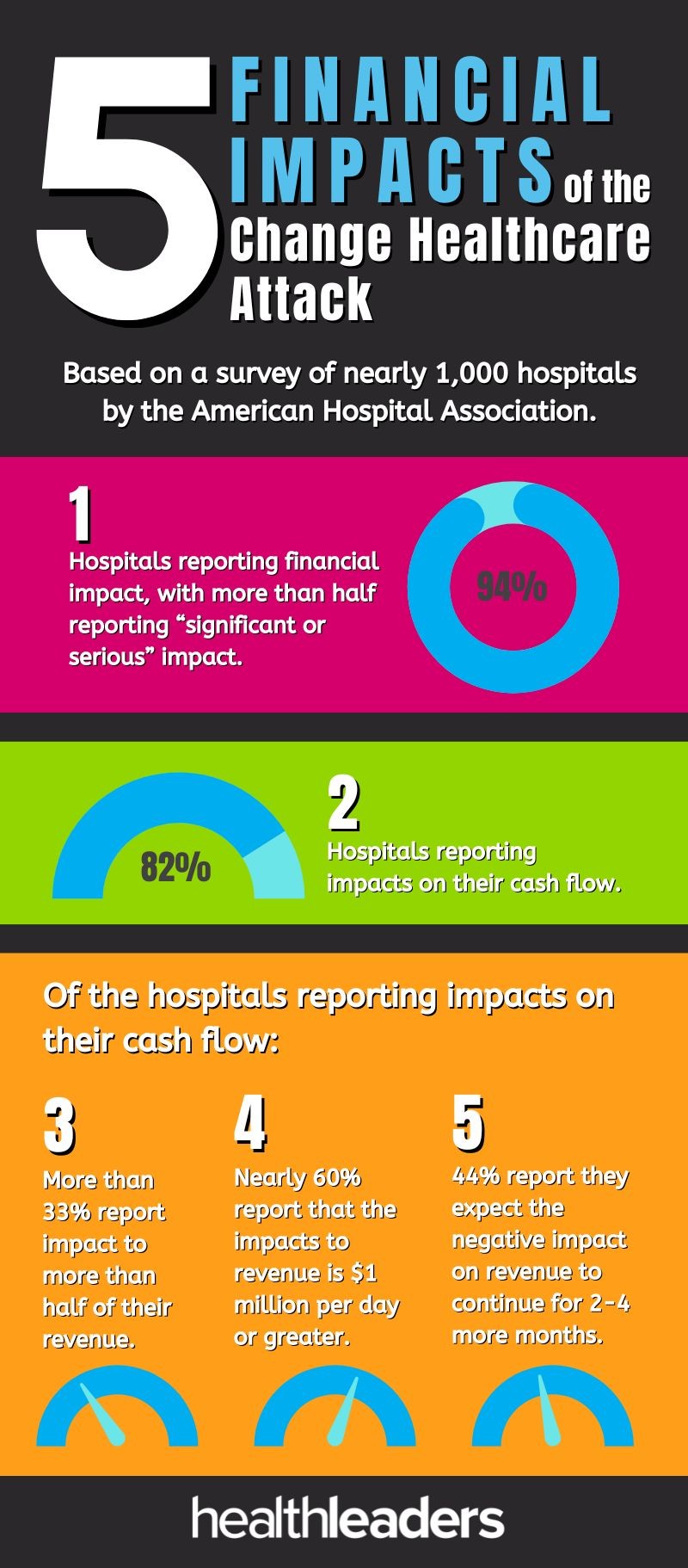

Change Healthcare processes 15 billion transactions annually and the lost payments from the attack are draining hospitals by the day. According to a survey by the American Hospital Association that collected responses from nearly 1,000 hospitals, 94% of operators are reporting financial impact, with more than half reporting “significant or serious” impact. Of the 82% of hospitals reporting impacts on their cash flow, nearly 60% report that the impacts to revenue is $1 million per day or greater.

It's never a good time for hospitals to be losing money, but the cyberattack has exacerbated the multiple financial challenges many operators have already been fighting. It’s creating somewhat of a perfect storm, Heywood stated.

“I coined that 2024 is going to be ‘the year of chaos.’ What I mean by that is you're going to have organizations that have had two to three years of financial issues really start struggle,” he said.

“You're going to have some of these issues with the for profits and hedge funds because the easy money is going away. And as that easy money goes away, the structures of some of those deals are not viable anymore. So you're seeing a lot of clean up and a lot of turmoil in 2024 and you're going to see it carry on in probably 2025, if not a little further out.”

The future is now

If there were any CEOs on the fence about investing in technology, especially on the cybersecurity and IT side, the Change Healthcare situation should have plenty reconsidering their stance.

When something is affecting the bottom line so drastically, hospital decision-makers have no choice but to re-strategize with the aim of both preventing future attacks and steadying the ship when it inevitably does occur.

“Hopefully it gets a lot of CEOs’ attention because they need to cross their T's and dot their I’s, close loopholes in their systems, and upgrade systems,” Ben Wobker, founder and CEO of Lake Washington Physical Therapy, told HealthLeaders. “It sounds like that's going to be the case here according to the headlines, but then again, you have to have that allocation of security spend and technology spend and make that a bigger budget line item.”

The AHA survey found that most hospitals are implementing workarounds to deal with the cyberattack, but those solutions are labor intensive and costly. Healthcare, as an industry, is known to be slow in implementing new technology, but with the rate tech is growing at, hospitals may not have much of a choice anymore for slow playing it.

Investment, of course, requires money and resources. That’s why Heywood believes it’s as important as ever to ensure you have some financial wiggle room to not only spend on technology, but to potentially throw capital at whatever is around the corner.

“You have to have a strong balance sheet,” he said. “You have to have cash on hand to be able to weather some of these storms that are coming. You're going to need to be in in this tight environment. You're going to need to be willing to spend money on cybersecurity and your IT. If you're already financially challenged, you do not want to be cutting your IT, your security, because that only further puts you in a bind.”

When it comes to dealing with the fallout of a cyberattack, however, technology is only one part of the equation.

You’re only as good as the systems you have in place and those systems aren’t immune to failure, Wobker noted. Updating and refreshing hardware and software should be the first step, but there also needs to be contingency plans in place to go offline.

Straying too far from traditional methods isn’t the answer either, according to Heywood.

“Now if you ask people to go back to paper, it's like, ‘Oh my gosh, I'm back in the stone age,’ he said. “So you have to have preparations to go back to paper in order to be able to get through a down time and you have to have backup systems so you could shut something down and turn it back on.”

There are few positives in the Change Healthcare attack, but the one silver lining may be the lessons that CEOs are forced to take away from it.

Whether it’s another cyberattack, pandemic, or anything else, those lessons should have hospitals better prepared for whatever is next.

Hospitals' bottom lines are under duress as a result of the crippling cyberattack.

The ramifications of the Change Healthcare cyberattack are wide-reaching, causing hospitals everywhere to weather the financial effects.

The subsidiary of UnitedHealth Group experienced the outage last month and since then, providers have had to pick up the pieces during a time when many organizations are already struggling with low operating margins.

Here’s a look at five numbers that illustrate the financial impact of the attack, based on survey responses from nearly 1,000 hospitals collected by the American Hospital Association:

Matt Heywood tells HealthLeaders what hospital leaders should consider when seeking out partnerships.

The current circumstances around healthcare are forcing hospitals to take a hard look at consolidation, maybe more than ever before.

Matt Heywood, CEO of Aspirus Health, is aware of that as much as anyone as the leader of a health system that just closed its own merger. Earlier this month, the Wausau, Wisconsin-based operator combined with Duluth, Minnesota-based St. Luke’s to create a 19-hospital organization that serves the systems’ two home states, as well as parts of Michigan.

The motivation behind a merger will differ depending on the health system, but Heywood believes that organizations should have a consistent approach to partnering if they want to get the most out of it—one that doesn’t over-leverage while also enabling a sense of urgency.

For Aspirus, the opportunity to combine with St. Luke’s allows the system to especially benefit on two fronts, Heywood told HealthLeaders.

“We knew as we were growing so fast that if we continue to make sure we held our company at a strong operating level, that we were able to look at other contiguous partners that would then help provide another tertiary center for us,” Heywood said. “We needed that other tertiary center because it would give us an ability to transfer patients within our service area somewhere else other than Wausau, which was already starting to get bottlenecked, and it would give some redundancy.”

The other area Heywood highlighted as benefiting from the merger is back-office capabilities, which he said will become more cost effective, safer, and more efficient. With the types of challenges facing hospitals these days, from financial stressors to cybersecurity, having stronger back-office functions can make all the difference on operating margins.

“We saw a lot of back-office synergies that we could provide by working with St. Lukes as well,” Heywood said. “So we're excited that by putting the two together, we can get that decompression of Wausau, we can get that back office, and we can improve the care for all our communities by being there for them when they need us.”

Matt Heywood, CEO, Aspirus Health.

In the case of many other health systems right now, financial distress is the catalyst for seeking out mergers. According to a recent report by Kaufman Hall, 28% of the 65 transactions announced in 2023 featured a partner under financial pressure, compared to 15% in 2022.

“What we're finding is that there are a lot of ‘have’ and ‘have-nots’,” Heywood said. “It was always there a little bit, but it's now really starting to separate. The people doing well are going to continue to do well and the ones not doing well will either have to make some tough choices to turn it around and some of them may or may not be able to do that, or be willing to do that, and the ones who can't are going to have to look at other alternatives and that might be a potential partner. This environment is going to create a potential increase in mergers over time.”

Making deals for the sake of dealmaking, however, isn’t a viable solution. The margin for error in transactions is decreasing, according to a recent report by Bain & Company, forcing organizations to consider whether potential deals are demonstrating enough value.

Proactively identifying the right partner is critical, Heywood stated. Even after finding one, the deal should be a fit for what you want to achieve.

“Don't just merge to merge,” he said. “You have to be willing to walk away from something that doesn't make sense.”

As a CEO, the job of carrying out a merger is far from finished once the deal is completed. Then comes the transition period, which is vital for getting your organization on track to be as efficient and effective as possible, as soon as possible.

“You have to actually get something from the merger and very fast,” Heywood said. “You can't do what a lot of companies do, which is merge, try to soft pedal, and tell everybody, ‘You know what, we don't want to change too much right now. We don't want to rock your world.’ You don't have that luxury, especially if the merger is a merger of individuals that may not be doing so well financially.

“You have to move fast to get the accretive value of a merger and you can't do what you used to do, which is just merge, take your time, and slowly do it. You have to be careful. You have to be thoughtful. But you have to be decisive and have some speed.”

CEOs should be all about purposeful action when it comes to M&A right now.

With that approach, dealmaking can be a fruitful strategy for both the ‘haves’ and 'have-nots’ in the fight against tight margins.

Keeping workers engaged allows leaders to potentially prevent staff from walking out the door.

It’s no secret that an engaged employee is more likely to stay at their place of work.

That’s why CEOs understand the importance of fostering engagement among their staff, which increases an organization’s chances of retaining talent and cutting down on turnover.

Retention remains a major challenge for leaders, with one in five workers who were at their organization in 2022 leaving the following year, according to Press Ganey’s “Employee experience in healthcare 2024” report.

The data is based on annual, pulse, and lifecycle surveyed that fielded responses from over 345,000 registered nurses and 131,000 physicians providers in 2023. Researchers measured employee engagement on an employee’s connection to and satisfaction with their workplace, intent to stay, and “likelihood to recommend” their employer.

Here are four employee engagement trends from the report.

General engagement is up, but..

Engagement took a hit during the pandemic when healthcare experienced an exodus of workers, but it’s now on the rise for the first time since then.

Thanks to nearly half of all healthcare roles improving on engagement over a year, general engagement jumped from 4.02 (out of five) to 4.04.

However, there’s still plenty of room for improvement, with nearly one-third of employees reporting low engagement in their workplace.

Nurse engagement is improving

Nursing has suffered some of the most turnover in recent years and forced CEOs to reconsider workplace strategies.

The good news for organizations is that clinical registered nurses saw the second-most improvement in engagement among all roles, climbing 0.04 to 3.89.

It’s a welcomed trend for CEOs who want to cut down on utilization of contract labor and expenses associated with turnover.

Leader engagement is dropping

On the opposite end, leader engagement continues to trend in the wrong direction.

Engagement among leaders has dipped three years in a row, dropping 3.7% during that period, representing one of the few roles which hasn’t started to rebound from the pandemic.

The trickle-down effect is that without engaged leaders to create and sustain engagement among their staff, workers across the organization will have little reason to be involved.

Generational differences

Engagement doesn’t just vary by role, but also by generation, with the data revealing a stark difference between older and younger workers.

Millennials, who now make up over one-third of the healthcare workforce, have an engagement experience of 3.89, compared to 4.12 among non-millennials.

CEOs should understand that the same strategies used to engage the previous generation of workers may not work with the next wave of employees. Appealing to the younger generation is critical though as more longtime workers exit the profession.

Solving for these challenges is a must for leaders to maintain a healthy bottom line.

Low operating margins at hospitals and health systems right now are the result of several factors that are giving CFOs headaches.

While margins have stabilized for many operators, certain drivers are putting immense pressure on health systems’ finances, forcing leaders to rethink and refine their strategies to stay out of the red.

Chief among those concerns is labor costs, according to a report from the Healthcare Financial Management Association (HFMA) and healthcare strategy and market research company Eliciting Insights.

The report reveals the biggest financial pain points for hospitals, based on survey responses of 135 health system CFOs and qualitative interviews with CFOs during the first quarter of the year.

Here are the top three causes of low operating margins cited by CFOs and how they can respond.

Higher labor costs

Chosen by nearly all respondents (96%), lowering expenses associated with the workforce remains a priority for health systems.

One of the primary reasons hospitals’ margins are suffering is due to the shortage of workers, especially nurses. Ninety nine percent of surveyed CFOs said that among all roles, nursing is experiencing the most shortage, followed by LPN/med tech nursing (75%), lab techs (74%), and radiology techs (73%).

By focusing on recruitment and retention, leaders can bolster a workforce that is both strong and sustainable. That entails investing in your staff by raising salaries to be commensurate with industry demand and offering creative benefits to keep employees happy.

Cutting down on turnover will also lessen hospitals’ reliance on contract labor, which was necessary during the COVID-19 pandemic but is now ballooning costs.

Organizations should also be putting resources into building up the next generation of workers through involvement in education.

Lower reimbursement from payers

After labor costs, reimbursement was the next biggest concern among surveyed CFOs, chosen by 84% of respondents.

Many leaders believe they aren’t being adequately reimbursed for services by payers, which is draining their finances. Taking a hard stance at the negotiating table can often be beneficial, but it may not always be possible.

So, what can CEOs and CFOs do? Some strategies include reducing costs without negatively affecting quality of care, allowing hospitals to not need a change in rates. Or, operators can consider adding speciality services that payers reimburse at a higher rate, which will also attract more patients seeking diverse types of care.

Maybe most importantly, however, leaders should establish a collaborative relationship with payers that is mutually beneficial. If payers see that you’re able to improve patient outcomes and do it in a cost-effective way, reimbursement will follow. Open communication will also create more transparency around rates, leading to more effective dialogue in negotiations.

Higher supply costs

Selected by 47% of surveyed CFOs, supply chain expenses finished ahead of lower inpatient volumes (25%), lower outpatient volumes (17%), and lower patient collections (10%) as the third-most pressing challenge.

To optimize the supply chain, CFOs should do value analysis on the products they’re currently using or products they’re considering switching to so they can understand how necessary the costs associated with those products are.

Can you use cheaper products that won’t impact quality of care? That simple change may have a significant impact on the bottom line.

The health system has sold several hospitals of late to improve its finances.

Tenet Healthcare’s selling spree has shown little sign of slowing down.

After recently divesting several assets, the for-profit health system continued its strategy by agreeing to sell two California hospitals to Adventist Health for approximately $550 million to further reduce its debt and improve its leverage position.

The transaction, which is expected to close in the spring, will send Sierra Vista Regional Medical Center and Twin Cities Community Hospital to Adventist and net Tenet after-tax proceeds of about $450 million and a pre-tax book gain of about $275 million. The operators also announced that they reached an agreement for Tenet’s subsidiary, Conifer Health Solutions, to provide revenue cycler services for Adventist.

Tenet has had a busy stretch as a seller. The system completed the sale of three hospitals in South Carolina to Novant Health for approximately $2.4 billion last month, while also agreeing to offload four hospitals in Southern California to UCI Health for about $975 million.

Tenet had agreed to sell San Ramon Regional Medical Center to John Muir Health as well, but that sale was tripped up by the Federal Trade Commission blocking the deal for eliminating competition in the area.

Speaking on the fourth-quarter earnings call last month, Tenet CEO Saum Sutaria said the system has “demonstrated thoughtful divestiture activity in a way that remains consistent with our strategy and enhances not just our leverage position, but our belief in our ability to generate free cash flow going forward.”

The sales were part of the reason for Tenet’s performance in the fourth quarter of 2023, which saw it beat Wall Street expectations and report net income of $244 million.

Selling off hospitals is allowing Tenet to turn its attention to its ambulatory care business. That segment experienced a 15.4% increase in net operating revenues in the fourth quarter compared to the same period in 2022.

As Tenet continues to reshape its business, more divestures could be in the works to create greater financial flexibility.

“Tenet is entering a new era, with a greater proportion of our performance coming from our highly efficient ambulatory surgical business and a reduced debt profile, we are well positioned to continue to expand free cash flow further over time,” Sutaria said.

To grow and sustain the business, leaders should be asking necessary questions about key facets of their financial strategy.

Hospitals across the country are under immense financial stress and as long as that fiscal pressure remains high, CEOs have no choice but to always be operating with the bottom line in mind.

Even as the median operating margin for hospitals continues to stabilize and we move further away from the pandemic, expense growth continues to outpace revenue for many facilities, widening the gap between profitable and struggling organizations.

To keep the doors open CEOs need to be constantly evaluating and revaluating key areas with the aim of achieving fiscal sensibility. That’s why this topic and its solutions will be featured in a roundtable discussion at our upcoming HealthLeaders CEO Exchange, held in May in Kohler, WI.

Attendees talk shop at the 2023 HealthLeaders CEO Exchange.

Until then, here are three ways CEOs can strive for fiscal sensibility:

Understand your market

Whether your hospital is thriving or not, it’s necessary for leaders to gauge their market and where they stand within it.

If your market is growing, it’s important to take advantage by broadening your reach to capture new patients. If your market is being compressed, you must find ways to hold onto your share, such as keeping referrals for speciality care.

Seeking out M&A is strategy for both growth and survival, with one of the trends in the dealmaking right now being health systems’ reorganization of regional markets. By committing resources to core markets with growth potential, health systems can expand delivery of care across their organization.

Assess revenue streams

One of the primary ways to combat high expenses is to introduce new revenue streams, but CEOs should first recognize what is and isn’t working for them currently.

If your hospital is finding success with digital health solutions, for example, consider how you can capitalize on patients’ needs by expanding your offering so you can provide care outside of your walls.

At the same time, many hospitals, especially in rural locations, are having to cut back on services because they’re not generating enough revenue to keep up with costs. A study by Chartis found that nearly a quarter of rural hospitals closed their obstetrics unit, while 382 have stopped providing chemotherapy.

Sometimes, scaling back or eliminating services will create more financial stability than adding new streams.

Improve payer relations

Costs ballooning at a faster pace than reimbursement will always be challenging for CEOs to navigate, which is why it’s as vital as ever to have a strong payer strategy.

Establish a relationship with payers that creates transparency, allowing you to know the rates they’re asking for and why. That will enable both parties to reach an agreed upon endpoint without wasting time and energy.

Rather than adding to the adversarial dynamic, leaders can benefit from a more collaborative approach that emphasizes open communication with payers, which can reduce administrative burden like denials.

Are you a CEO interested in attending our event and strategizing with other attendees? To inquire about attending the HealthLeaders Exchange event, email us at exchange@healthleadersmedia.com.

The HealthLeaders Exchange is an executive community for sharing ideas, solutions, and insights. Please join the community at our LinkedIn page.